- •“Is Bitcoin Dead?” searches surge during drawdowns, but rising volumes also reflect a growing and more aware investor base.

- •ETF flows, financialization, and macro stress are shaping the narrative more than any protocol-level failure.

- •Bitcoin’s system remains operational; the debate now centers on its role within an increasingly institutional market structure.

So we are back to the same question: is Bitcoin dead? This is something we see start surging in volume every time Bitcoin experiences drawdowns. The moment price weakens and momentum fades, the narrative shifts from optimism to doubt.

Looking at the latest data from Google Trends, we are seeing a surge in search queries containing phrases like “is Bitcoin dead” and “Bitcoin going to zero”, levels that were last seen during the 2022 bear market. And in almost every bear cycle, we see new records in these search volumes. As more people become aware of and invested in Bitcoin, each bear market attracts a larger audience, which naturally pushes search volumes to new highs. Concerns reach their highest point when Bitcoin starts showing no signs of immediate recovery.

So instead of discussing whether Bitcoin is dead or not, the more important discussion is this: why there is so much negativity, and what trends are fueling this narrative.

Google Trends Shows Record “Bitcoin Is Dead” Searches

First, let’s look at this logically. On Google Trends, search queries for “Bitcoin is dead?” are surging and have broken previous all time highs. But why?

An increase in search queries does not automatically signal panic. It can also reflect a larger and more aware user base. More people are invested in Bitcoin today. More people follow its price. So when drawdowns occur, more participants are searching for answers.

Around a year ago, institutions like BlackRock and Vanguard were actively promoting their Bitcoin ETFs. That activity increased exposure and brought new capital and new attention into the market. With a broader audience tracking Bitcoin, price declines naturally generate more online discussion and more search volume.

Drawdowns themselves are not new for Bitcoin. Looking at previous cycles:

2011: -93%

2013: -83%

2017: -84%

2021: -73%

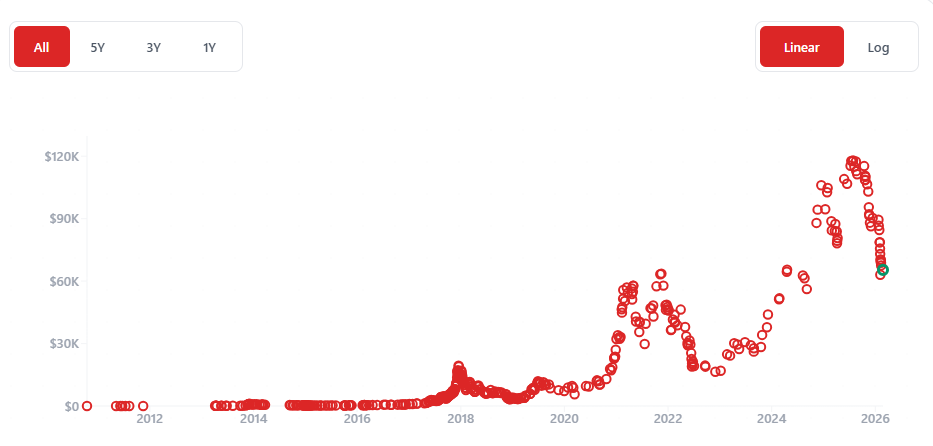

In 2026, from the most recent all time high, Bitcoin has seen a drawdown of roughly 55%.

If we look at the pattern objectively, the magnitude of drawdowns has generally decreased over time. That suggests structural changes in market composition, including a larger and more diversified holder base. This cycle also includes institutional participation, which did not exist at scale in earlier periods.

The key point is this: data should guide the discussion. Market emotions are loud, but they are not always aligned with long term structural shifts.

And this is not the first time people have been skeptical and searching for whether Bitcoin is dead. In fact, there is an entire website dedicated to tracking every time Bitcoin has been declared dead since 2010, when it was trading at just $0.11.

Structural and Narrative Forces Behind the “Bitcoin Is Dead” Cycle

Let’s look at the current sources of FUD around Bitcoin to understand what is happening in the market and what the data tells us.

The “Supercycle” Thesis

First, we need to address the supercycle narrative. This idea was not only promoted by several crypto influencers, but also publicly discussed by CZ, the founder of Binance.

The thesis suggested that Bitcoin typically follows a four year cycle, largely influenced by the halving event. However, supporters of the supercycle argument claimed that Bitcoin no longer needed to follow this traditional structure. The reasoning was that new market participants, particularly institutional capital, could extend or even break the four year cycle.

Under this view, expectations shifted toward a delayed peak, with projections pointing to a new all time high in late 2025 or even 2026.

In reality, much of this narrative functioned as hopium. It kept conviction high and delayed the acceptance of downside risk. However, as the recent drawdown unfolded, with Bitcoin declining from its all time high back toward levels seen around the time of the U.S. presidential transition, confidence in the supercycle thesis weakened significantly.

Quantum Threat

Another narrative gaining traction is the quantum computing threat. The argument is simple. If quantum computing advances to a point where it can break current cryptographic standards, Bitcoin’s security model, which relies on algorithms like ECDSA, could theoretically be compromised. While this risk is still considered long term, institutions do not price risk based only on probability. They also price it based on potential impact.

We have already seen cautious adjustments.

In early 2026, Jefferies strategist Christopher Wood removed a 10% Bitcoin allocation from his “Greed & Fear” model portfolio and reallocated it toward physical gold and mining equities. The reason cited was quantum computing risk. This reflects a preemptive de-risking approach, effectively applying a higher risk premium to Bitcoin exposure.

Kevin O’Leary also talked about how many institutions may cap Bitcoin allocations at around 3% of portfolios until quantum risks are better understood or mitigated. According to him, this limitation is tied to fiduciary responsibility rather than short term price expectations.

BlackRock has not reduced exposure. However, it expanded quantum risk disclosures in the prospectus for its iShares Bitcoin Trust ETF in 2025. This signals institutional awareness, even if no allocation changes have occurred.

There is another structural concern. Even if the broader Bitcoin network upgrades to quantum-resistant cryptography and most holders migrate their funds to protected wallets, early wallets that have never moved, including the Satoshi-era wallets holding roughly 1.1 million BTC, could remain exposed. If those coins were ever compromised, the supply shock alone would create significant market instability.

The issue, therefore, is not immediate collapse. It is uncertainty. And in financial markets, uncertainty alone is enough to influence positioning and narrative.

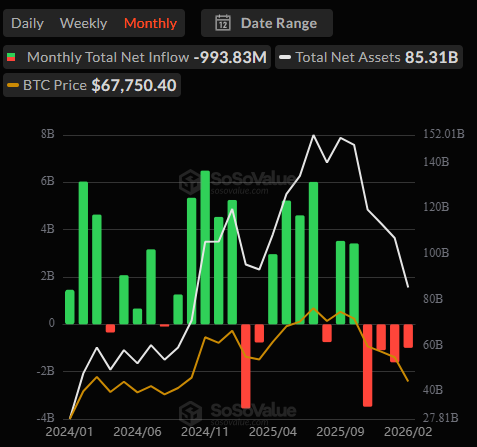

ETF Flows

If we look at the current cycle objectively, the bull run effectively began after the first U.S. spot Bitcoin ETFs were approved on January 10, 2024. Following that approval, we saw unprecedented institutional demand. ETF inflows were recorded among the strongest launches in ETF history.

After Bitcoin, we also saw additional crypto-related ETFs being approved, including Ethereum, and later products tied to assets like XRP and Solana. This marked a structural shift in how crypto exposure was being packaged and distributed to traditional investors.

However, sentiment began to shift around October 10, the day the market experienced one of its largest liquidation events in recent memory. While there are multiple theories behind that move, no single confirmed trigger exists. Since then, Bitcoin ETF flows have turned negative at different intervals.

For many newer participants, ETF outflows are being interpreted as a signal of weakening institutional conviction. Whether that interpretation is fully accurate or not, the optics matter. When inflows were strong, they reinforced the bullish narrative. When flows turn negative, the narrative adjusts accordingly.

Financialization of Bitcoin

Another major theme this cycle is the financialization of Bitcoin. Bitcoin began as a decentralized peer to peer alternative to traditional finance. Over time, however, it has become increasingly integrated into the same system it was meant to operate outside of.

This shift accelerated in 2017 with CME futures and intensified after spot ETFs were approved in 2024, bringing tens of billions in institutional inflows. Today, Bitcoin exposure exists through ETFs, futures, options, structured products, and corporate treasury allocations.

Supporters argue this increases legitimacy and liquidity. Critics argue it raises correlation with traditional markets and introduces systemic risks, shifting Bitcoin from a parallel system into a macro asset competing with gold and equities.

That said, Bitcoin is not unique in this transformation. As assets grow, institutions build financial tools around them. The question is not whether financialization is happening. It is whether this process strengthens Bitcoin’s role in global markets or changes its original incentives in ways that create new risks.

Store-of-Value Stress Test

The “Store-of-Value stress test” is another narrative gaining attention this cycle. Bitcoin was built for an environment marked by geopolitical tensions, inflation concerns, and currency debasement. It has often been grouped alongside gold and silver, positioned as “digital gold”, and in many cases presented as a superior alternative. Fixed supply. Portability. Verifiability.

However, the current macro environment has created divergence. While gold and silver have rallied strongly, Bitcoin has experienced a significant drawdown from its 2025 peak. Precious metals have absorbed capital flows during periods of uncertainty, reinforcing their traditional safe haven role. Bitcoin, on the other hand, has traded more in line with risk assets, particularly during liquidity tightening and de-risking events.

This divergence has led to renewed questioning of the store-of-value thesis. If Bitcoin is meant to hedge against inflation and macro instability, why has it not consistently behaved like gold during recent stress periods?

Part of the answer may lie in its financial integration. With ETFs and derivatives, Bitcoin is now more embedded within institutional portfolios, increasing its correlation with broader markets. Instead of operating outside the system, it now competes within it as a macro asset.

The stress test, therefore, is straightforward: during periods of uncertainty, does Bitcoin attract defensive capital, or does it move with broader risk sentiment?

So Is Bitcoin Really Dead?

There are many other narratives in play. OG Bitcoin holders exiting. Regulatory tightening. Every month, a new wave of FUD emerges.

But the more important questions are technical.

– Is the protocol broken?

– Has the network stopped producing blocks?

– Has the monetary policy changed?

– Has the hash rate collapsed permanently?

If the system itself is still operating as designed, then debating whether Bitcoin is “dead” becomes more about sentiment than structure.

Historically, Bitcoin has been declared dead hundreds of times. The counter currently stands at 467 declarations. The first time it was declared dead, Bitcoin was trading at around $0.11. At the 467th declaration, it is trading near $64,000, regardless of where the all time high stands. That contrast alone puts the narrative into perspective.

And if, after looking at that historical pattern and understanding the risks, someone still chooses to gain exposure, the practical side matters. Execution, liquidity, and trading costs play a role. Platforms like Bitunix, for example, offer competitive fees and deep liquidity for traders seeking efficient Bitcoin exposure without unnecessary slippage.

Institutions may be adding risk premiums. Allocations may be more measured. Regulation may be increasing. But capital continues to engage with the asset class. Bitcoin is no longer operating outside the financial system. It is now embedded within it.

The question is no longer about survival. It is about how Bitcoin positions itself within a maturing market structure.